Corporate earnings have a more nuanced effect on stock price movements than many realize, with market reactions often unfolding over time.

Referring to the mighty Efficient Market Hypothesis (EMH), you might expect stock prices to adjust immediately to earnings surprises. But most often, real-world stock price behavior tells a very different story: a sharp initial move that's followed by a predictable drift.

As of August 1, 2025, roughly 66% of S&P 500 companies had reported Q2 earnings, with 82% beating EPS estimates, and 80% surpassing revenue forecasts. This happened despite a shaky market spooked by tariffs. Yet despite about 6.4% average EPS growth year-over-year, stocks typically only moved about 1.9% on announcement day.

This only signals what market analysts have observed for years: markets digest some of the surprise immediately, but a larger share of the price moves happens gradually over days, weeks, or even months. The evidence dates back to the late 1960s.

Markets digest some of the surprise immediately, but a larger share of the price moves happens gradually over days, weeks, or even months.

Let's explore why this may be the case and the not-so-simple relationship between earnings surprises and stock price moves.

The expectation game sets the stage

When companies report results, what has the maximum impact on stock prices is not the raw performance reflected in the earnings numbers in absolute terms, but the performance relative to what the market expected. So, in case the market had lower expectations (through conservative guidance or selective leaks), it becomes easier to beat them. If a company, for instance, reports a 15% decline in earnings, but analysts had anticipated a 20% drop, the actual result is seen as better than expected.

Some firms even time discretionary expenses like R&D to deliver surprise beats. At the same time, while consensus estimates dominate headlines, whisper numbers ( an unofficial, often higher, earnings expectation making rounds among large investors and traders ) often set the true expectations. So, you can expect standout stock price moves only when earnings beat the whisper rather than the consensus numbers. On the flipside, underperforming the whisper, despite a consensus beat, can lead to a muted stock movement.

Let's say two companies each beat consensus by 10%. One also beats the whisper estimate, while the other fails to do so. So, which stock do you expect to jump more? Empirical data shows that it's almost always the one that beats the whisper. Financial analysts have observed that beating both layers of investor expectation: the consensus estimate and the whisper number, has led to an average 2% or higher intraday jump.

Financial analysts have observed that beating both layers of investor expectation: the consensus estimate and the whisper number, has led to an average 2% or higher intraday jump.

Three phases of price moves surrounding corporate results

Phase 1: Movements before results

P rices often start drifting before the earnings numbers hit the market. Stocks typically rise ahead of positive surprises and slip ahead of disappointments. According to a study by Friedman & Zeng, this pre-announcement drift is less powerful in retail-heavy stocks, where sentiment-driven activity can cloud the trend. This may suggest a shift in institutional positioning ahead of results.

Phase 2: The earnings days

On the earnings day, expectations meet reality, and it brings clarity (or confusion, as there is so much information to deal with). According to FactSet, companies that delivered positive earnings surprises saw their stock prices rise an average of 2.4% in the trading window spanning two days before to two days after the earnings release. Conversely, companies reporting negative surprises faced a sharper price move, with average declines of 3.5% during the same period. Yes, negative news has a stronger effect.

According to FactSet, companies that delivered positive earnings surprises saw their stock prices rise an average of 2.4% in the trading window spanning two days before to two days after the earnings release.

That said, how far prices move depends not only on the surprise magnitude, but also on tone (this is where AlphaPro's Earnings Sentiment score comes into play) . Confident, forward-looking commentary strengthens upside moves while a vague or cautious tone can mute it despite a company reporting good numbers.

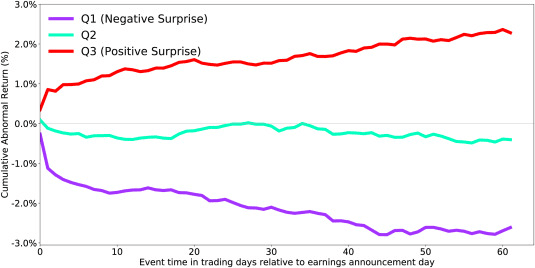

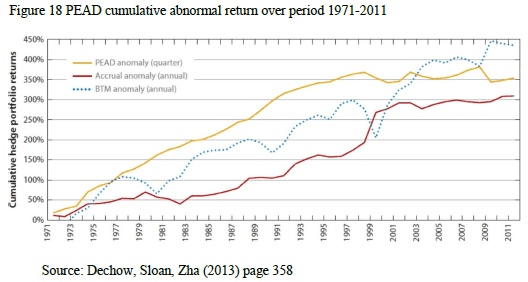

Phase 3: Post‑Earnings Announcement Drift (PEAD)

The most interesting and consequential price moves take place in the Post‑Earnings Announcement Drift (PEAD) phase. It is a phenomenon, first identified by Ball & Brown (1968) and later documented by Bernard & Thomas (1990), where stocks continue moving in the direction of the surprise (positive or negative) for weeks or months afterward. Early research documented quarterly abnormal returns of approximately 8-9%, which translates to an annualized return of around 30%. More recent studies incorporating both EPS and revenue surprises estimate annualized returns from this drift to be between 7.6% and 12.5%.

This means in phase 1, whispers and sentiment set the stage, and in phase 2, actual results and tone deliver the plot twist. Finally, in phase 3, the market digests, debates, and reprices gradually over time.

And, PEAD is stronger in small/mid‑caps and retail-heavy names

Unsurprisingly, PEAD tends to show more pronounced effects in retail-heavy stocks where analyst and institutional coverage is not as intense . Small-cap and mid-cap firms often fit this description, leading to slower price discovery over weeks and even months. One possible reason is that retail investors are often slower to react to information that has a bearing on the stock price.

The key takeaways are that pre-earnings moves are powered mainly by institutional investors, while retail investors, who account for nearly one-fifth of US stock trading volume, generally enter the picture later.

Surprise is a signal, not noise

Earnings seasons come with a multilayered narrative of expectation, tone, sentiment, and timing. To interpret the story correctly, you need to read past the consensus, tune to whisper sentiment, gauge earnings sentiment, and follow the drift curve. Blindly reacting to earnings surprises alone won't help you stay on the right side of the market moves.