Buying the dip has become one of investing's most trusted rules of thumb. Knowing when not to buy may be the more valuable skill.

The three most dangerous words in investing might be these:

One piece of investment advice that has become almost second nature over the past two decades is buying the dip. Every market decline is followed by a flood of opinions on why it may be a great buying opportunity. With markets making new highs so frequently in recent years, the idea has become even more ubiquitous.

History has also given plenty of reasons to think in that way.

The dot-com crash eventually gave way to a new bull market, and so did the global financial crisis. The pandemic-induced sell-off of 2020 turned out to be the shortest bear market on record. Investors who had the conviction to buy while others were selling were eventually handsomely rewarded. Even the sharp 2022 correction now looks far less frightening in hindsight than it did at the time.

Looking back, it is easy to see why so many investors have come to believe that every decline eventually becomes tomorrow's buying opportunity. Investors have seen enough recoveries over the years that every new decline begins to resemble the last one, even when the reasons behind it are completely different.

But history also shows that treating every dip the same can be just as costly as ignoring every opportunity.

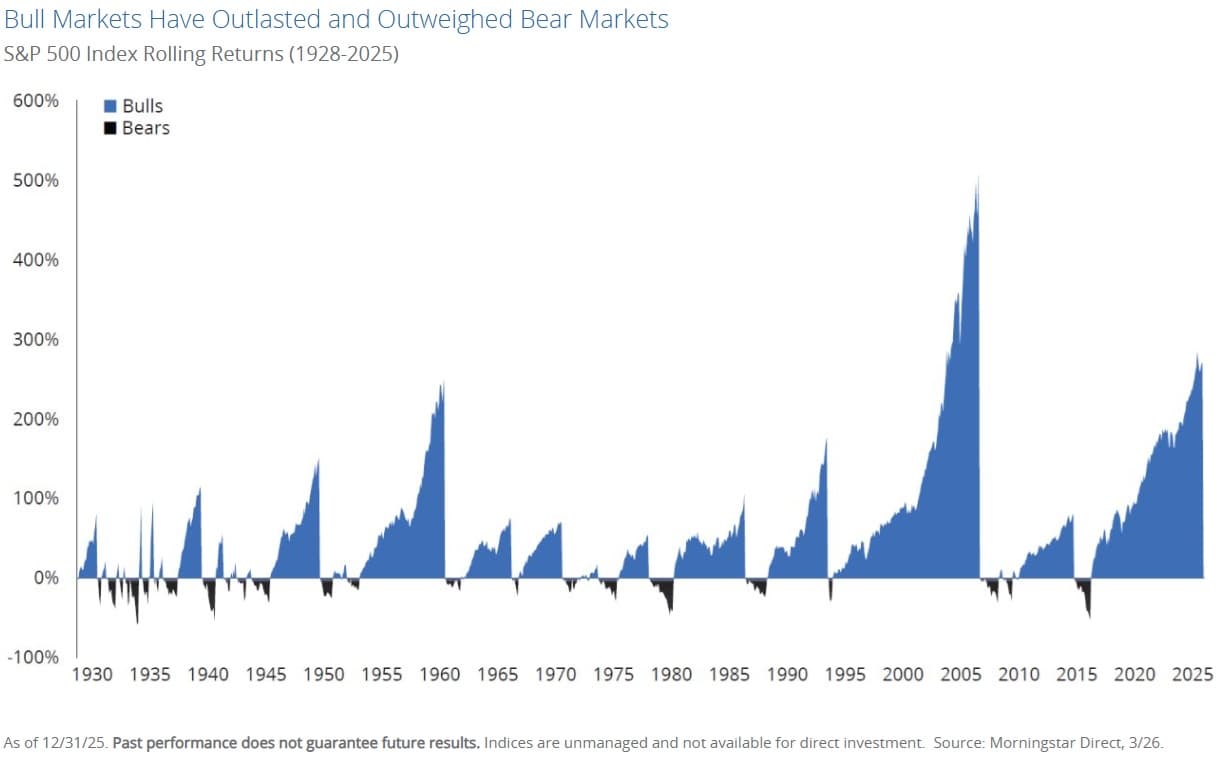

Mighty Bulls, Tiny Bears

One reason has become so widely accepted is that the market has done an extraordinary job of rewarding patience. Since 1928, the S&P 500 has gone through 27 bear markets. The average decline has been about 35%, and the average bear market has lasted just under ten months.

Bull markets, by comparison, have lasted almost three times as long (992 days or 2.7 years) and have generated average gains of nearly 114%. Looking at those numbers alone, it is difficult to argue against buying when prices fall. History appears to be firmly on the side of investors willing to tolerate short-term pain in exchange for long-term returns.

The difficulty is that those numbers describe markets, not individual stocks.

A broad market index like the S&P 500 isn't static. Companies that stop growing are replaced by those that do, which means the index that eventually recovers may contain a very different collection of businesses from the one that originally fell. Investors remember that the S&P 500 eventually climbed back to new highs, conveniently ignoring how few of yesterday's market leaders ever made it there.

The problem is that has become an umbrella term for decisions that have very little in common. Buying into a broad market sell-off is very different from averaging down on an individual stock. The first is largely a bet on the resilience of the economy over long periods of time. The second is a judgement about the future of a specific business. Past records suggest those two decisions should not be treated as though they carry the same odds.

Most Stocks Never Become Great Investments

One of the easiest mistakes to make after a sharp decline is to assume that a lower price automatically makes a stock a better investment. Sometimes it does, but more often, this intuition has limits.

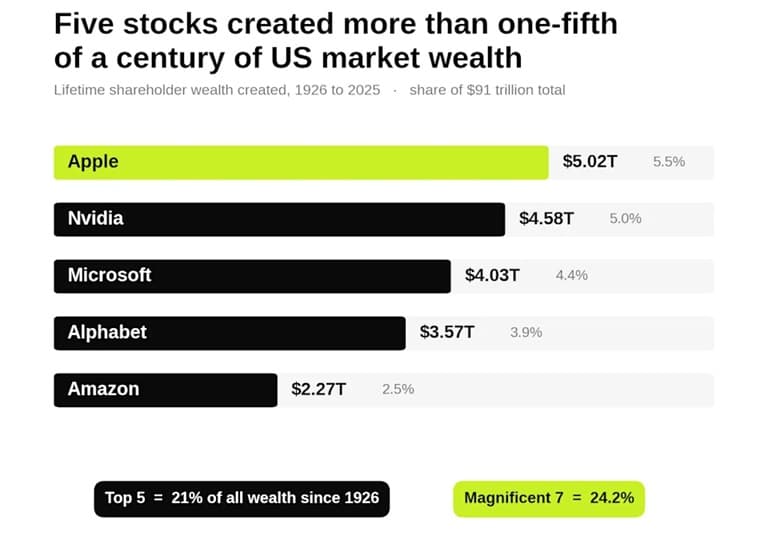

Hendrik Bessembinder, a finance professor at Arizona State University, recently updated one of the most widely cited studies on long-term stock market returns. Examining nearly 29,800 US-listed companies over the hundred years from 1926 to 2025, he found that almost 60% of all stocks actually reduced shareholder wealth over their lifetimes.

Even more revealing, just 46 companies (roughly 0.2% of all listed stocks) accounted for half of the $91 trillion in net wealth created by the entire US stock market over that century. The broader pattern has remained remarkably consistent across his research: only a tiny fraction of companies create the overwhelming majority of long-term shareholder wealth. In his earlier work, roughly 4% of listed stocks accounted for virtually all of the market's net wealth creation.

That finding changes the way we think about buying the dip.

If most companies never go on to become extraordinary investments in the first place, there is little reason to assume that a falling share price, by itself, improves the odds. A stock trading 40% below its previous high may represent an opportunity, but so are the odds that the business had its best years already behind it.

There is no shortage of examples.

Investors who bought the early declines in Kodak spent years watching a dominant business lose relevance as digital photography replaced film. Nokia looked inexpensive after its first major sell-off, yet the smartphone revolution permanently altered its competitive position. BlackBerry followed a similar path.

The stocks of these companies didn't lose their value overnight. For many investors, each successive decline looked like another buying opportunity rather than evidence that the underlying business itself was changing.

The Difference Between Cheap and Cheaper

Investors often spend so much time talking about prices and so little time talking about businesses. A falling share price is more likely to create an impression that something important has happened to the stock. But looking at price charts alone, it's not immediately obvious what that something is. It can happen because of several factors or combinations of multiple factors.

A company may have lost customers because a competitor may have introduced a better product. Growth may simply be returning to more normal levels after years of euphoric expectations. There may be a change in management. Sometimes none of those things has happened, but investors have simply become worried about the economy, inflation, interest rates, or geopolitical events.

So, how does one separate the from the bad ones?

A reliable way of separating one from another is to forget the decline for a moment and return to the original investment thesis. That also needs a shift of attention from price movement to the business itself.

Would you still be comfortable buying this company considering the fundamental factors: the company's ability to generate cash, defend its market position, finance its obligations, and keep earning attractive returns over long periods of time?

Another key question to ask is whether the decline is company-specific or simply part of a much broader market correction. A stock that fell alongside the rest of the market during a recession or a geopolitical shock is more likely to recover as those conditions normalize.

But a stock that keeps falling while the broader market has already recovered is a different case altogether. In the latter case, it usually has less to do with investor sentiment and considerably more to do with the business itself.

A lower share price is often a perfectly good reason to pay attention to a stock. But does it deserve a place in your portfolio? Answering that question requires looking well beyond the share price. The key thing to find out is whether the business itself remains as strong as the one that commanded a higher price only a short while ago.