At times, markets behave in counterintuitive ways. They might fall on rate cuts or rally on rate hikes. And sometimes, the market ignores interest rates like a cat ignores its owner until it's dinner time.

Yet despite being so crucial for modern economic life, very few investors truly understand how interest rate changes have a ripple effect on the stock market. Interest rates decide how much it costs to borrow, how much you earn by saving, and how financial markets value every future dollar a company promises to make. When interest rates move, different economic sectors may expand or shrink. Bond markets also respond as investor psychology shifts.

The interest rates–stock market connection goes far beyond the simple rule To understand the effects of interest rate changes on stocks, we need to start with basic economics. The real story gets more interesting when we walk through the history, the academic research, and the data that tie interest rate movements to market behavior.

The Economics: Why Changing the Price of Money Changes Everything

Imagine a business deciding whether to build a new factory. When interest rates are low, it's cheaper to borrow, which makes future earnings more attractive and valuations richer. Conversely, higher interest rates make borrowing expensive, which makes future profits look smaller. Naturally, investors would demand higher returns to hold risky assets like stocks. This is the key logic at the heart of valuation models: the higher the rate, the lower the present value of future cash flows, which pushes valuations down.

Beyond valuations and return expectations, interest rate changes affect the real economy in several ways. The moment a central bank hikes rates, consumer spending slows because it's now costlier to borrow and spend. Higher rates also push businesses to reconsider expansion or hiring plans. Bond yields climb, as higher rates lead to lower prices for existing bonds. So, when suddenly pays 5%, equities have to justify their higher risks.

What History Shows: Markets and Rates Move Together More Often Than We Think

Eugene Fama, the economist behind the Efficient Market Hypothesis (EMH), spent decades trying to understand how markets digest information. One of the things his research kept pointing back to was that markets don't just react to interest rates; they react to what those rates imply about the future economy. In several of his well-known papers, Fama found that when expected inflation rises (something you can often see through short-term rates or yield spreads), future stock returns tend to weaken.

In simple words, when interest rates rise, it puts pressure on equity valuations, because future company earnings now get discounted more heavily, and investors now want a larger return for taking the risk. Essentially, Fama's work underscored that the information contained within the interest rate changes — rather than the changes themselves — is what moves the market.

This idea didn't stay theoretical as, over the years, plenty of research has tried to measure how macro expectations (whether they show up in inflation signals or interest-rate moves) actually shape stock returns.

One of the earliest came from Fama himself, in a 1977 paper with G. William Schwert titled Stock Returns, Real Activity, Inflation, and Money. Using U.S. data from the 1950s through the early 1970s, they showed that periods of rising expected inflation tended to coincide with weaker stock returns. The key insight wasn't that inflation mechanically pushes stocks down, but that rising inflation usually signals slower real economic activity and higher required returns. In other words, macro expectations — not just company fundamentals — play a powerful role in how markets price the future.

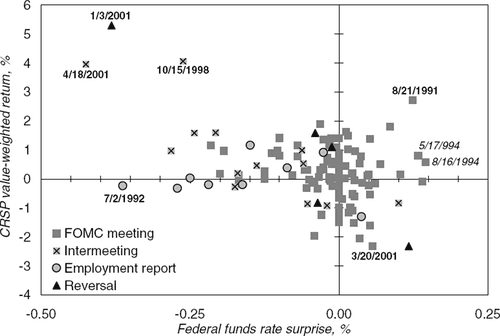

Decades later, research became even more precise. In 2005, Ben Bernanke and Kenneth Kuttner published a landmark study titled "What Explains the Stock Market's Reaction to Federal Reserve Policy?", which examined every Federal Reserve policy announcement from 1989 to 2002.

By using Fed funds futures to isolate the portion of each rate decision, they found that the stock market reacts far more strongly to unexpected rate moves than to planned ones. A surprise rate hike reliably pushed stocks lower, while an unexpected cut often produced sharp gains.

When a rate change was fully anticipated, markets barely reacted. Some of the key findings of the paper were:

- Unanticipated changes in the federal funds rate target had an immediate and statistically significant effect on equity markets.

- An unexpected 25-basis-point cut in the federal funds rate was associated with approximately a 1% increase in broad stock indexes.

- The market's reaction was primarily due to the policy's effect on expected future excess returns (the equity premium), rather than changes in the real interest rate or future dividends.

A broader, global view comes from a 2018 IMF working paper, which examined 20 advanced economies over nearly four decades. The researchers found that markets react very differently depending on the economic backdrop. When central banks raised rates because growth was strong and the economy was running hot, stock returns often remained positive. But when rates were lifted in a weakening economy to control inflation, it weighed heavily on the equity markets.

The Data Modern Investors Should Understand

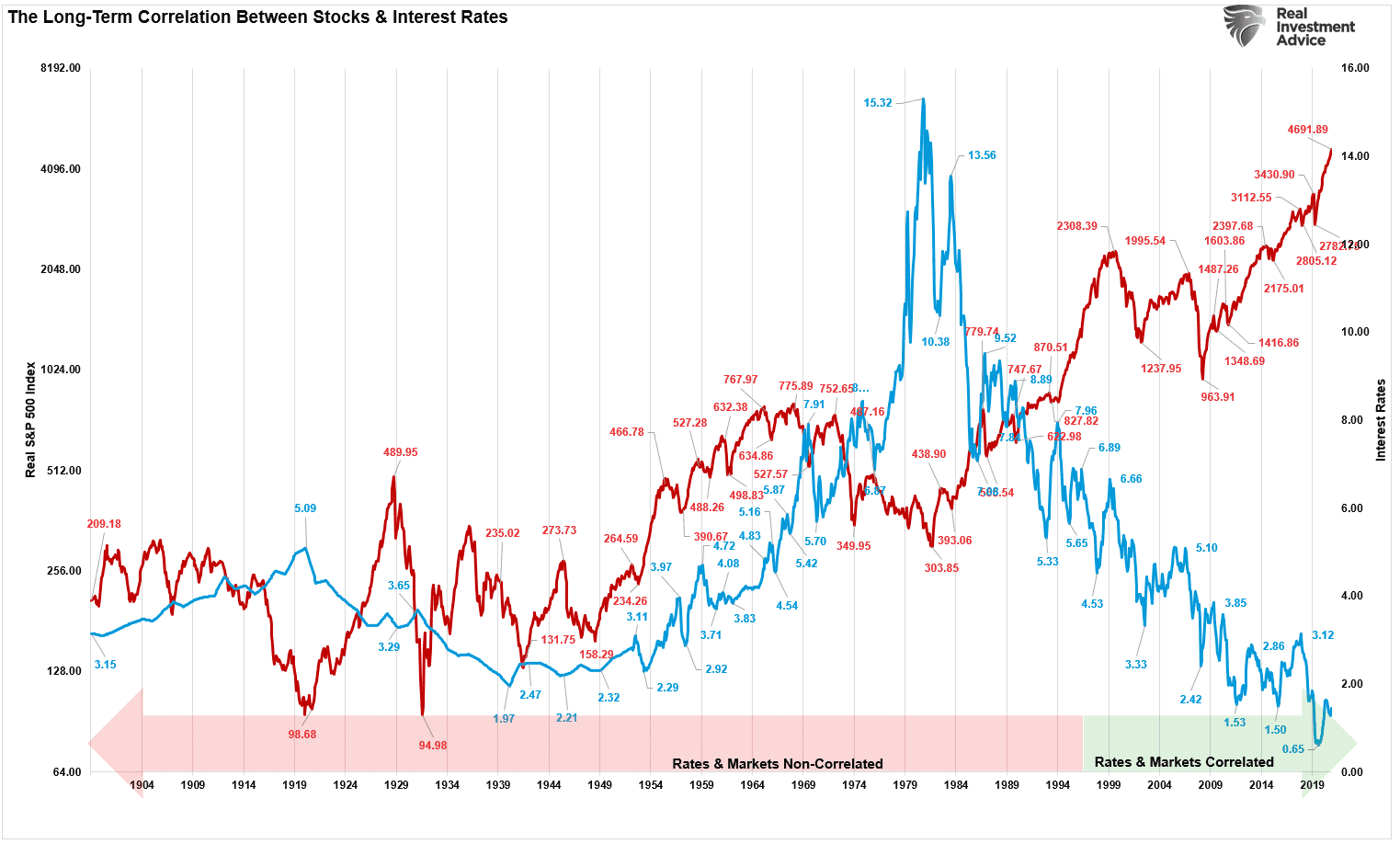

If you overlay the federal-funds rate with the S&P 500 over the last half-century, you can see a clear story. In the early 1980s, policy rates were in double digits; by the late 1990s and 2000, rates had trended down to low single digits, and stocks delivered one of the great multi-decade bull runs. The long decline in yields helped fuel a sustained era of risk-taking and price rise.

Now, if we flip the tape back to the 1970s, you can see the market pulling off a completely different stunt. Runaway inflation and sharply higher rates led to what we call the for equities, when valuations nosedived and real returns were poor.

In 2013, when the Fed hinted that it would taper bond purchases, it triggered the As 10-year Treasury yields jumped from roughly mid-1s to about 3% over a few months, the VIX Index spiked in June and October 2013, reaching levels above 20 from a low of around 12 in early May. But equities ultimately managed to hold up because of resilient corporate earnings. That episode showed markets react to the larger context of interest rate changes rather than the headline rate itself.

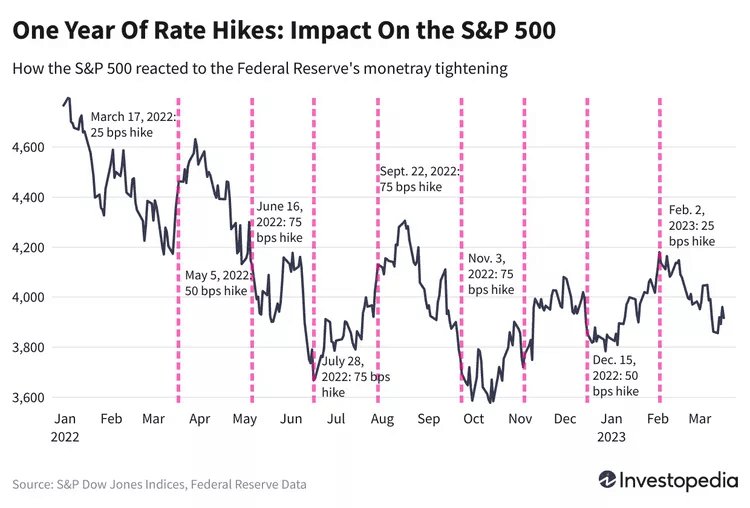

Contrast that with 2022, when the Fed acted faster than it had in decades to lift policy rates from zero bound to the mid-4s within a year. The market's reaction was nothing short of dramatic. The S&P 500 finished the year down about 19-20% while the Nasdaq plunged roughly a third. High-growth companies felt the biggest impact, since so much of their value comes from profits expected years down the line.

Additionally, time-varying models in academic literature find that the impact of rate moves depends on context: hikes in an overheated economy often do less harm than hikes when the economy falters. A recent paper (Time-varying influence of interest rates on stock returns: evidence from China, Gu, Zhu & Wang, 2021) shows interest-rate impacts on stocks are not constant; they change with the macro backdrop. And asymmetric-effect studies across China, Turkey, Indonesia, South Africa, and elsewhere find that markets often react more strongly to rate increases or surprises than to equivalent cuts.

Why Some Rate Hikes Kill Markets And Others Don't

By now, one thing is clear: rate changes affect the market significantly, but not all rate changes are equal. This is why we need to consider rate changes along with economic contexts and investor expectations.

Consider this: In 1994, the Federal Reserve raised interest rates aggressively. The federal funds rate was increased by 250 basis points (from 3.0% to 5.5%) through a series of hikes within that year, with the cycle ending at 6.0% in early 1995. Yet the stock market barely flinched. The reason the market didn't stumble despite aggressive rate hikes was that corporate earnings growth smoothed the blow.

Now contrast that with late 2022 when rate hikes happened at a time when earnings were slowing down, liquidity was drying up, and inflation was at a multi-decade high. So even fundamentally strong companies took a hit because the discount rate moved so violently.

This is why investors who simply memorize misunderstand the market. More than anything, interest rates are signals and, like any signal, they need to be studied in economic context.

Where Rates Hit Hardest: Growth, Leverage, Real Estate

The effects of rates are not evenly spread across all corners of the market.

High-growth tech stocks, whose valuations depend on far-future earnings, are often the most sensitive ones. Their cash flow duration is long, so a higher discount rate slices their valuations sharply. This may make Nasdaq look like a leveraged bet on interest rates.

Companies with heavy debt loads also struggle because refinancing gets expensive. Real estate investment trusts, homebuilders, and companies with large capital requirements tend to feel rate pressure before the rest of the market.

Meanwhile, banks sometimes benefit from rising rates, at least up to a point, because their net interest margins expand. But history shows that if rates rise too quickly, credit risk often offsets the benefit.

Yes, nothing in the market moves in a straight line following a simple rulebook!

So What Should Investors Actually Do with All This?

First things first: to understand interest rates, investors don't need to try guessing what's going to happen in the next Fed meeting. That game belongs to hedge funds with teams of economists and models running around the clock. Most investors don't need to forecast rates at all. What's more important is understanding what rising or falling rates mean for the environment you're investing in.

If rates are going up slowly while the economy is strong, history shows the market can usually absorb that hike without much volatility. But if rates are jumping quickly while the economy is not on the right track, it makes sense to be cautious.

And sometimes, it's not the rate move itself that shakes the market, but how the move compares to what investors were expecting. As Yahoo Finance explains, stock prices can swing sharply when expectations diverge from the Fed's decision. If investors believe the Fed should have cut rates and it doesn't, stocks can fall. If they believe the Fed should have raised rates and it holds steady, stocks can rise. Or as David Russell of TradeStation puts it, "The Fed's main impact on the stock market is to confirm or reject expectations about rates and the economy."

Conclusion: Interest Rates Are the Market's Most Honest Whisper

Every investor eventually finds out that the market is shaped less by noise and more by forces that move under the surface. Interest rates are one of those forces. They determine how money flows, how future earnings of companies are valued, and how risk can be weighed.

A rate cut or a hike, therefore, should never be taken in isolation. The more important factor to consider is what led to the interest rate policy change, the economic backdrop, the expectations, and the surprises. In short: read the rate environment right, and you'll read the market right.